Business

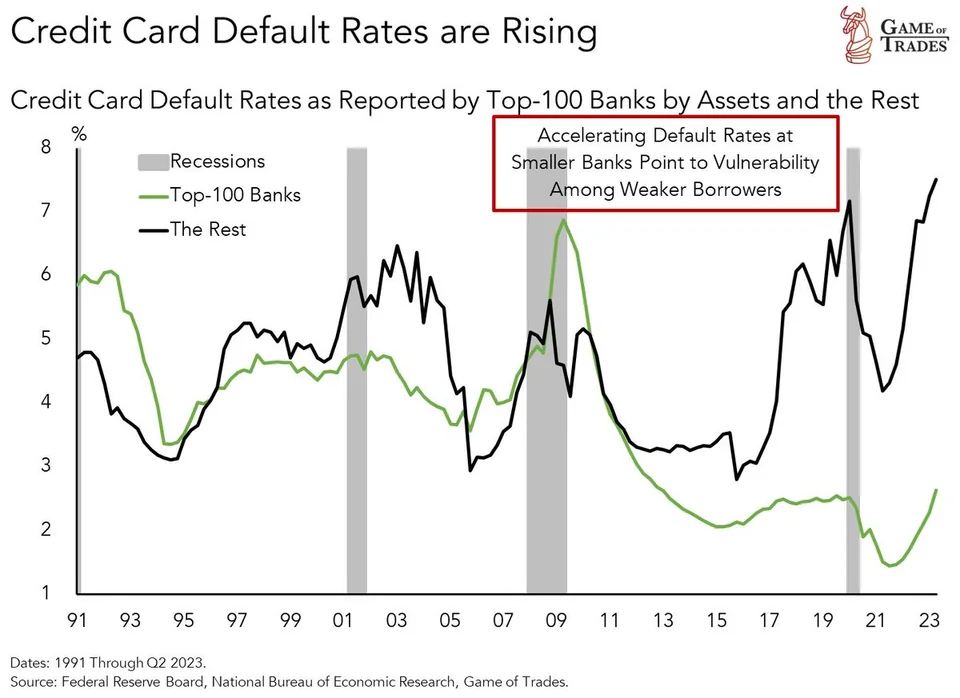

Credit Card Default Rates Surge: Top 100 Banks At 2.45%, Rest Hit All-Time High OOf 7.51%

(CTN News) – In the constantly evolving realm of the financial sector, the concern over credit card default rates has taken center stage.

Recent data highlights a striking trend: default rates among the top 100 banks sit at a relatively modest 2.45%, while the rest of the financial institutions grapple with a staggering 7.51%.

This surge in default rates is the highest ever recorded, prompting critical questions about the state of consumer finances and the broader economy.

In this blog post, we will explore the factors contributing to this unprecedented rise and its implications for both banks and consumers.

Credit Card Default Rates

Credit card default rates indicate the percentage of credit card accounts that have become delinquent for 90 days or more, signifying that cardholders have failed to meet their payment obligations as agreed.

These rates serve as a crucial gauge of both consumer financial health and the stability of the banking sector.

The Top 100 Banks vs. Others

The stark contrast in default rates between the top 100 banks and the remaining financial institutions is a cause for concern. The top 100 banks, with their lower default rate of 2.45%, seem to have weathered the storm more effectively.

However, it’s vital to note that even this lower rate carries significance, particularly considering the economic challenges stemming from the COVID-19 pandemic.

In contrast, the rest of the banks grapple with a default rate of 7.51%, more than three times higher than that of the top 100 banks.

This disparity suggests that smaller and regional banks may face unique challenges in maintaining the creditworthiness of their cardholders.

Factors Driving the Surge

Several factors contribute to the alarming rise in credit card default rates:

- Economic Uncertainty: Lingering effects of the pandemic have created an environment of economic uncertainty, with job losses, income instability, and rising inflation leaving many consumers struggling to meet their financial obligations.

- Lending Practices: Some banks may have adopted more lenient lending practices during the pandemic, leading to a higher risk of defaults among their cardholders.

- Credit Card Debt: Consumers carrying high levels of credit card debt are particularly vulnerable to defaults, especially if they encounter unexpected financial challenges.

- Interest Rates: Higher interest rates on credit card balances can make it harder for consumers to repay their debts, thereby leading to more defaults.

Implications for Banks and Consumers

For banks, the surge in credit card defaults carries significant financial implications. Higher default rates can result in increased provisions for bad debt, impacting their profitability.

Banks may also become more cautious about extending credit, making it harder for consumers to access credit cards or secure favorable terms.

Consumers, on the other hand, should exercise caution and prudence in managing their credit card debt. Avoiding high balances, making timely payments, and seeking financial advice when needed can help mitigate the risk of default.

The unprecedented rise in credit card default rates, particularly among smaller banks, is cause for concern. It reflects the challenges consumers face in an uncertain economic climate.

As the financial landscape continues to evolve, both banks and consumers must adapt to ensure the responsible use of credit cards and maintain financial stability.

Monitoring the situation closely and seeking strategies to navigate these challenging times successfully remains crucial for both parties.

The Impact of Your Credit Card Interest Rate When it comes to interest rates, securing the lowest possible rate is always a wise financial decision.

On the surface, the difference between a 15% APR and a 20% APR may appear modest, but if you maintain a revolving balance on your credit card, a lower interest rate can potentially save you thousands of dollars.

Let’s illustrate this with an example.

Comparison of Credit Card Interest Costs

- Credit Card Balance: $7,500

- Monthly Payment: $150

- Interest Rate (APR) 15%

- Months to Pay Off Debt: 78

- Total Interest Paid: $4,145

- Credit Card Balance: $7,500

- Monthly Payment: $150

- Interest Rate (APR) 20%

- Months to Pay Off Debt: 106

- Total Interest Paid: $8,254

Of course, the ideal way to manage credit cards is to pay off your balance in full every month. If you can establish this habit and avoid accumulating credit card debt, the APR on your account won’t affect your budget at all.

In fact, paying off your full statement balance monthly allows you to avoid credit card interest charges entirely.

How to Reduce Your Credit Card Interest Rate

If you’re working on paying down credit card debt, securing a lower interest rate can help you save money and accelerate your debt reduction.

Here are several strategies to consider for lowering your credit card APR:

- Balance Transfer: You may be eligible to open a new credit card offering a low-rate or 0% APR balance transfer promotion. While these introductory interest rates typically last for 12 to 18 months, aggressively tackling your debt during this period can significantly reduce or even eliminate your credit card debt.

- Using a balance transfer calculator can help you account for transfer fees, introductory rates, and more to calculate potential savings. It’s advisable to compare multiple balance transfer credit card offers to find the best fit for your situation. Keep in mind that you generally need good to excellent credit to qualify for these offers.

- Consolidation Loan: Another option is to pay off your existing credit card debt with a debt consolidation loan. Depending on factors such as your credit score, debt-to-income ratio, and more, you might qualify for a personal loan with a lower interest rate than what you’re currently paying on your credit cards.

- A low-rate debt consolidation loan can save you money and expedite the debt repayment process. Additionally, by consolidating your revolving credit card debt into an installment loan, you could reduce your credit card utilization rate, potentially improving your credit score.

- Request a Lower Rate: Remember that your credit card APR isn’t set in stone. You can reach out to your credit card issuer and inquire about the possibility of lowering your interest rate. In some cases, your request may be successful.

- When making your request, inform the issuer if you’ve received credit card offers with lower interest rates that you’re considering. Having a history of on-time payments on your account and a good credit score can also work to your advantage when negotiating a rate reduction.

Business

PepsiCo Reduces Revenue Projections As North American Snacks And Key International Markets Underperform.

(VOR News) – In the third quarter of this year, Pepsi’s net income was $2.93 billion, which is equivalent to $2.13 per share. This was attributed to the company.

This is in stark contrast to net income of $3.09 billion, which is equivalent to $2.24 per share, during the same period in the previous year. The company’s earnings per share were $2.31 when expenses were excluded.

Net sales decreased by 0.6%, totaling $23.32 billion. Organic sales increased by 1.3% during the quarter when the effects of acquisitions, divestitures, and currency changes are excluded.

Pepsi’s beverage sales fell this quarter.

The most recent report indicates that the beverage and food sectors of the organization experienced a 2% decline in volume. Consumers of all income levels are demonstrating a change in their purchasing habits, as indicated by CEOs’ statements from the previous quarter.

Pepsi’s entire volume was adversely affected by the lackluster demand they encountered in North America. An increasing number of Americans are becoming more frugal, reducing the number of snacks they ingest, and reducing the number of times they purchase at convenience stores.

Furthermore, Laguarta observed that the increase in sales was partially attributed to the election that occurred in Mexico during the month of June.

The most significant decrease in volume was experienced by Quaker Foods North America, which was 13%. In December, the company announced its initial recall in response to a potential salmonella infection.

Due to the probability of an illness, the recall was extended in January. Pepsi officially closed a plant that was implicated in the recalls in June, despite the fact that manufacturing had already been halted.

Jamie Caulfield, the Chief Financial Officer of Pepsi and Laguarta, has indicated that the recalls are beginning to have a lessening effect.

Frito-Lay experienced a 1.5% decline in volume in North America. The company has been striving to improve the value it offers to consumers and the accessibility of its snack line, which includes SunChips, Cheetos, and Stacy’s pita chips, in the retail establishments where it is sold.

Despite the fact that the category as a whole has slowed down in comparison to the results of previous years, the level of activity within the division is progressively increasing.

Pepsi executives issued a statement in which they stated that “Salty and savory snacks have underperformed year-to-date after outperforming packaged food categories in previous years.”

Pepsi will spend more on Doritos and Tostitos in the fall and winter before football season.

The company is currently promoting incentive packets for Tostitos and Ruffles, which contain twenty percent more chips than the standard package.

Pepsi is expanding its product line in order to more effectively target individuals who are health-conscious. The business announced its intention to acquire Siete Foods for a total of $1.2 billion approximately one week ago. The restaurant serves Mexican-American cuisine, which is typically modified to meet the dietary needs of a diverse clientele.

The beverage segment of Pepsi in North America experienced a three percent decrease in volume. Despite the fact that the demand for energy drinks, such as Pepsi’s Rockstar, has decreased as a result of consumers visiting convenience stores, the sales of well-known brands such as Gatorade and Pepsi have seen an increase throughout the quarter.

Laguarta expressed his opinion to the analysts during the company’s conference call, asserting, “I am of the opinion that it is a component of the economic cycle that we are currently experiencing, and that it will reverse itself in the future, once consumers feel better.”

Additionally, it has been noted that the food and beverage markets of South Asia, the Middle East, Latin America, and Africa have experienced a decline in sales volume. The company cut its forecast for organic revenue for the entire year on Tuesday due to the business’s second consecutive quarter of lower-than-anticipated sales.

The company’s performance during the quarter was adversely affected by the Quaker Foods North America recalls, the decrease in demand in the United States, and the interruptions that occurred in specific international markets, as per the statements made by Chief Executive Officer Ramon Laguarta.

Pepsi has revised its forecast for organic sales in 2024, shifting from a 4% growth rate to a low single-digit growth rate. The company reiterated its expectation that the core constant currency profitability per share will increase by a minimum of 8% in comparison to the previous year.

The company’s shares declined by less than one percent during premarket trading. The following discrepancies between the company’s report and the projections of Wall Street were identified by LSEG in a survey of analysts:

SOURCE: CNBC

SEE ALSO:

Old National Bank And Infosys Broaden Their Strategic Partnership.

(VOR News) – Old National Bank, a commercial bank with its headquarters in the Midwest, and Infosys, a firm that specializes in information technology, have recently entered into a strategic expansion of their link, which has been in place for the past four years.

This expansion is more likely to take place sooner rather than later, with the likelihood being higher.

For the purpose of making it possible for Old National Bank to make use of the services, solutions, and platforms that are offered by Infosys, the objective of this expansion is to make it possible for the bank to transform its operations and processes through the application of automation and GenAI, as well as to change significant business areas.

This lets the bank leverage Infosys’ services, solutions, and platforms.

Old National Bank Chairman and CEO Jim Ryan said, “At Old National, we are committed to creating exceptional experiences for both our customers and our fellow employees.”

This statement is applicable to Old National Bank. Infosys is carefully managing the business process innovations that it is putting us through, putting a strong emphasis on efficiency and value growth throughout the process to ensure that it is carried out efficiently.

This is a routine occurrence throughout the entire operation. Because of Infosys’ dedication to our development and success, we are incredibly appreciative of the assistance they have provided.

Old National has been receiving assistance from Infosys in the process of updating its digital environment since the year 2020, according to the aforementioned company.

Ever since that time, the company has been providing assistance. The provision of this assistance has been accomplished through the utilization of a model that is not only powerful but also capable of functioning on its own power.

Infosys currently ranks Old National thirty-first out of the top thirty US banks.

This ranking is based on the fact that Old National is the nation’s largest banking corporation.

It is estimated that the total value of the company’s assets is approximately fifty-three billion dollars, while the assets that are currently being managed by the organization are valued at thirty billion dollars.

Dennis Gada, the Executive Vice President and Global Head of Banking and Financial Services, stated that “Old National Bank and Infosys possess a robust cultural and strategic alignment in the development, management, and enhancement of enterprise-scale solutions to transform the bank’s operations and facilitate growth.”

This remark referenced the exceptional cultural and strategic synergy between the two organizations. Dennis Gada is the one who asserted this claim. This was articulated explicitly concerning the exceptional cultural congruence and strategy alignment of the two organizations.

We are pleased to announce that the implementation of Infosys Topaz will substantially expedite the transformation of Old National Bank’s business processes and customer service protocols. We are exceedingly enthusiastic about this matter. We are quite thrilled about this specific component of the scenario.

Medium-sized banks operating regionally will continue to benefit from our substantial expertise in the sector, technology, and operations. This specific market segment of Infosys will persist in benefiting from our extensive experience. This phenomenon will enable this market sector to sustain substantial growth and efficiency benefits.

SOURCE: THBL

SEE ALSO:

American Water, The Largest Water Utility In US, Is Targeted By A Cyberattack

States Sue TikTok, Claiming Its Platform Is Addictive And Harms The Mental Health Of Children

Qantas Airways Apologizes After R-Rated Film Reportedly Airs On Every Screen During Flight

The largest regulated water and wastewater utility company in the United States stated Monday that it had been the target of a cyberattack, forcing the company to halt invoicing to consumers.

American Water, The Largest Water Utility In US, Is Targeted By A Cyberattack

American Water, based in New Jersey and serving over 14 million people in 14 states and 18 military facilities, said it learned of the unauthorized activity on Thursday and quickly took precautions, including shutting down certain systems. The business does not believe the attack had an impact on its facilities or operations and said employees were working “around the clock” to determine the origin and scale of the attack.

According to their website, American Water operates over 500 water and wastewater systems in around 1,700 communities across California, Georgia, Hawaii, Illinois, Indiana, Iowa, Kentucky, Maryland, Missouri, New Jersey, Pennsylvania, Tennessee, Virginia, and West Virginia.

SOURCE | AP

-

News3 years ago

News3 years agoLet’s Know About Ultra High Net Worth Individual

-

Entertainment2 years ago

Mabelle Prior: The Voice of Hope, Resilience, and Diversity Inspiring Generations

-

Health3 years ago

Health3 years agoHow Much Ivermectin Should You Take?

-

Tech2 years ago

Tech2 years agoTop Forex Brokers of 2023: Reviews and Analysis for Successful Trading

-

Lifestyles2 years ago

Lifestyles2 years agoAries Soulmate Signs

-

Movies2 years ago

Movies2 years agoWhat Should I Do If Disney Plus Keeps Logging Me Out of TV?

-

Health3 years ago

Health3 years agoCan I Buy Ivermectin Without A Prescription in the USA?

-

Learning2 years ago

Learning2 years agoVirtual Numbers: What Are They For?